ECB Financial Stability Risk Dashboard—2025

Euro Area Systemic Risk Overview

Executive Summary

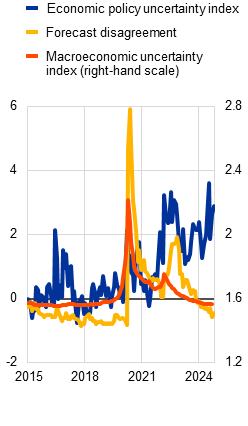

The ECB’s Financial Stability Review (Nov 2024) highlights persistent macro-financial and geopolitical uncertainty, with risks shifting from inflation to growth. While euro area banks remain resilient, vulnerabilities are rising in sovereign, corporate, and non-bank sectors. Market volatility and policy uncertainty remain elevated.

Key Risk #1

Macro-financial/geopolitical shocks & market volatility

Key Risk #2

Sovereign and corporate debt sustainability

Key Risk #3

Non-bank financial sector liquidity & leverage

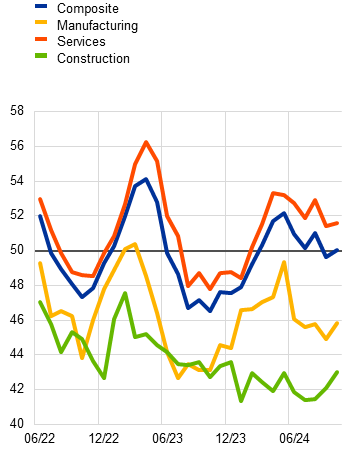

Macro-Financial & Market Environment

Uncertainty remains high due to geopolitical tensions and shifting monetary policy. Market volatility has increased, with sharp corrections in equity and bond markets. Policy rates remain elevated, and central bank balance sheets are gradually normalizing.

Market Volatility

Global Interest Rate Environment

Central Bank Balance Sheets

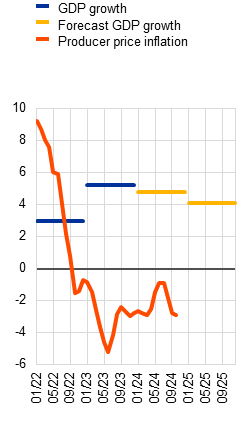

Economic Growth Forecasts

The European Commission has significantly cut its growth forecasts for the Eurozone as US trade policy creates economic disruption. The EU executive now expects the 20-member currency area's economy to grow only 0.9% in 2025—down from its previous estimate of 1.3%—and has reduced its 2026 GDP growth outlook to 1.4% from 1.6%.

Revised Growth Forecasts by Country

| Country | Previous 2025 Forecast (%) | Revised 2025 Forecast (%) |

|---|---|---|

| Eurozone (Overall) | 1.3 | 0.9 |

| Germany | 0.7 | 0.0 |

| France | 0.8 | 0.6 |

| Italy | 1.0 | 0.7 |

Source: European Commission Forecast, May 2025

Key Vulnerabilities by Sector

Household Sector

Household debt-to-income ratios have declined, but debt service costs remain elevated for some. Risks are concentrated among low-income and highly indebted households.

Corporate Sector

Corporate balance sheets are under pressure from high funding costs and weak growth, especially in commercial real estate and SMEs. Insolvencies are rising from low levels.

Sovereign & Market Risks

Sovereign vulnerabilities are increasing, especially in high-debt countries. Market volatility has increased, with sharp but short-lived corrections in equity and bond markets.

Banking Sector

Euro area banks remain resilient, with strong capital and liquidity buffers. Asset quality is deteriorating slowly, mainly in CRE, SMEs, and consumer credit, but exposures are manageable in aggregate.

Capital Adequacy by Country Group

Non-Performing Loan Ratio Trends

Stress Test CET1 Ratio Impacts by Country Group

Liquidity Metrics by Bank Type

European Banking Profitability Trends

European Banking System Risk Assessment by Country

Non-Bank Financial Sector

NBFIs face valuation, liquidity, and leverage risks, especially in investment funds and insurers. High concentration in equity holdings and increased exposure to US assets amplify vulnerabilities.

Climate & Emerging Risks

Climate change and transition risks are increasingly relevant for euro area financial stability. Physical and transition risks are sector-specific and evolving.

Evolution of Climate Risk Channels

Climate Risk Exposure by Economic Sector

Download Data

All charts and data from this report are available for download in multiple formats.

Further Resources

Related Risk Reports

ECB Financial Stability Review—2024

Official ECB assessment of euro area financial stability, risks, and resilience.

Macroprudential Bulletin

ECB bulletin on macroprudential policy, systemic risk, and regulatory developments.

Climate Risk & Financial Stability

Analysis of climate-related risks to euro area financial stability.